Reconciliation, payment execution, and reporting are shifting from batch processing to API-connected operations. Here’s what’s driving adoption and what implementation looks like for growth-stage platforms.

The financial operations layer in most ERP platforms still runs on infrastructure designed for batch processing. Bank statements arrive periodically. Reconciliation happens after data collection. Payment files get uploaded for processing. Reporting reflects historical snapshots.

That model worked when financial data moved slowly. It creates friction when clients expect continuous visibility.

According to Open Banking Limited, over 17 million people in the UK now actively use Open Banking services. For ERP platform operators, that adoption signals infrastructure maturity and an opportunity to rethink how financial workflows function.

The shift extends beyond technology. It’s fundamentally operational.

The payment economics problem

For B2B-focused platforms, percentage-based payment fees create ongoing cost pressure that doesn’t exist in consumer contexts.

A £50,000 supplier payment processed at 1.5% represents £750 in transaction fees. For platforms processing hundreds or thousands of such transactions monthly, these costs accumulate rapidly.

One payroll platform operator described the calculation: “Payment processing costs had become a material operational expense. The question was whether alternative infrastructure could address both cost and workflow efficiency simultaneously.”

Open Banking’s account-to-account payment infrastructure can, in some cases, shift cost structures away from higher percentage-based fees to lower percentage or flat-fee models, depending on the use case and volume. The cost difference becomes particularly material at B2B transaction scales.

But the operational case extends beyond payment costs. The more significant shift involves reconciliation and reporting workflows.

From scheduled reconciliation to event-driven matching

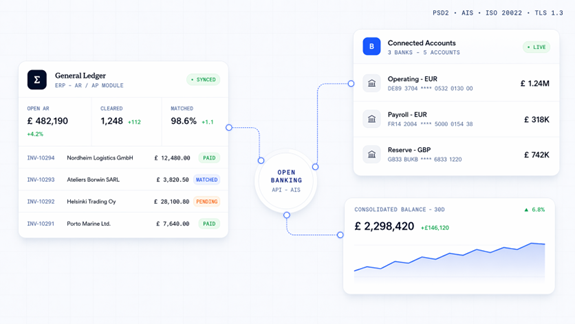

Traditional reconciliation operates on fixed cycles. Finance teams export bank statements periodically, import them into the ERP, match transactions manually against records, and investigate discrepancies.

Open Banking’s Account Information Services (AIS) infrastructure enables a different model: event-driven reconciliation triggered by transaction completion rather than calendar schedules.

Platform operators implementing this approach report material reductions in manual matching workload often redirecting substantial reconciliation capacity to higher-value financial analysis rather than data entry.

One finance director described the operational change: “Reconciliation shifted from a scheduled month-end task to something happening continuously. The team focuses on investigating exceptions rather than manual matching.”

The workflow transformation creates client-facing value. Discrepancies surface more quickly. Support inquiries related to reconciliation can decrease materially. Financial reporting reflects more current state.

Payment execution: from files to APIs

Payroll and AP workflows have historically required generating payment files, uploading them to banking portals, and waiting for batch processing. often three to five days for settlement.

Open Banking’s Payment Initiation Services (PIS) can replace file-based workflows with API-driven execution.

One payroll platform operator noted: “We moved to API-based payment initiation and started receiving immediate confirmation or error notifications. The visibility and control changed significantly.”

Platform operators report payment errors identified at initiation rather than during downstream processing, potentially reducing client friction and support burden. Settlement timelines may accelerate depending on implementation, improving working capital visibility for end clients.

Reporting: from snapshots to continuous data

Financial reporting in many ERP systems relies on periodic data imports. Weekly or monthly bank statement downloads. Batch processing. Reports generated from point-in-time snapshots.

Direct bank connectivity through Open Banking infrastructure changes underlying data timeliness.

Platform operators implementing this report more current balance and transaction data, cash flow reporting based on fresher information, and forecasting informed by more up-to-date transaction patterns.

According to Open Banking Limited’s impact assessment research, Open Banking-enabled services have generated an estimated £1.4 billion in economic value for UK SMEs — much of it through improved financial visibility.

One UK accounting platform serving 300+ SME clients implemented Open Banking connectivity in 2024. Over the subsequent 90 days, they reported reconciliation-related support inquiries decreased substantially, average reconciliation cycles shortened materially, and client satisfaction scores improved measurably.

What’s driving adoption now

Platform operators cite three primary drivers for Open Banking integration:

Cost pressure. Payment processing economics at B2B scales. Percentage-based fees on high-value transactions create material operational expense that alternative infrastructure models may address.

Client expectations. End users increasingly expect real-time financial visibility, automated workflows, and current data. Batch-based infrastructure struggles to deliver these experiences.

Platform operators integrating earlier gain operational experience ahead of broader market adoption. The timing question is strategic as well as technical.

Open banking providers serving growth-stage platforms

Several infrastructure providers have developed services specifically for growth-stage ERP, accounting, and payroll platforms serving UK based clients.

Finexer is one such provider. The company’s approach includes:

Unified infrastructure. A single API combining bank transaction data access (AIS) and payment initiation (PIS) capabilities. Platform operators report this consolidation can reduce integration complexity compared to managing multiple vendor relationships.

Agent-based access. Platforms may operate as an agent under Finexer for specific services. This allows access to bank data and payment capabilities within an approved framework. Platform operators note this can simplify access while still operating within regulatory requirements.

Bank coverage. Finexer’s infrastructure connects across a range of UK banks, including business accounts and challenger banks, addressing varied banking relationships of SME clients.

Deployment approach. Implementation timelines are designed to align with SaaS product development cycles. Platform operators report deployment timelines that may be shorter than some enterprise-oriented implementations, though actual timelines depend on platform complexity and technical requirements.

Commercial model. Finexer’s pricing scales with transaction volume rather than imposing fixed enterprise commitments, which may align better with growth-stage platform economics.

Ravi Ranjan, Finexer’s CEO, describes the positioning: “We built Finexer after observing a recurring pattern: platform operators understood the operational value of real-time financial workflows, but existing infrastructure options didn’t always align with their scale, timelines, or commercial model. We focused on addressing those specific requirements.”

Platform operators cite the combination of regulatory access pathway, deployment expectations, bank coverage, and commercial structure as relevant factors in infrastructure provider selection — particularly when evaluating fit with their operational scale.

About Finexer

Finexer is an FCA-authorised Open Banking infrastructure provider (FRN: 925695) in the UK, offering API access to bank transaction data (Account Information Services) and payment initiation capabilities (Payment Initiation Services).

Its infrastructure enables ERP, accounting, payroll, and PropTech platforms to connect to UK bank accounts, retrieve financial data, and initiate account-to-account payments within an established regulatory framework.

Finexer supports connectivity across a broad set of UK banks, including high street and challenger institutions, and provides integration models aligned with the operational requirements of scaling platforms.