How software companies can create a tax compliance strategy

The very nature of software taxability creates the perfect storm of complexity, contradictions, and challenges, which makes compliance near impossible to comprehend, never mind master. It’s no wonder software executives often fail to give tax compliance proper attention, focusing instead on more top-of-mind priorities like accelerating growth and maximizing efficiency.

But that’s old-school thinking. Sales tax compliance is no longer independent of growth and efficiency; it’s necessary to achieve both. The tax landscape has shifted dramatically, and software companies must up their game when it comes to tax compliance. Without a solid plan in place to address these changes, software companies face:

- Inefficiency due to time and resources spent on tax compliance

- Error-prone tax filings due to holes in compliance processes

- Reduced growth due to a negatively impacted IPO, merger, or acquisition slowed or undone by tax compliance issues uncovered during due diligence

The good news is that, when done right, sales tax compliance can propel your business. In short, doing sales tax right isn’t just an obligation or a way to avoid auditors, but a strategy for protecting growth.

The rules for taxing software products and services are complicated and ever-changing. Getting it right is difficult and resource intensive. Having a strategy in place to manage sales tax compliance is key. This guide provides foundational insight to help you:

- Create a more efficient, less costly, and less resource-intensive process for managing sales and use tax

- Confidently go after new market or revenue opportunities without adding tax risk

- Adopt a scalable, sustainable sales tax strategy that supports growth goals

How company growth creates tax risk

In some ways, the software industry is a victim of its own innovation and success. With so many high-growth companies in software, state and local governments see opportunity and are evolving their tax policies to shore up growing deficits, targeting the very activities that enable these businesses to expand at such a rapid pace.

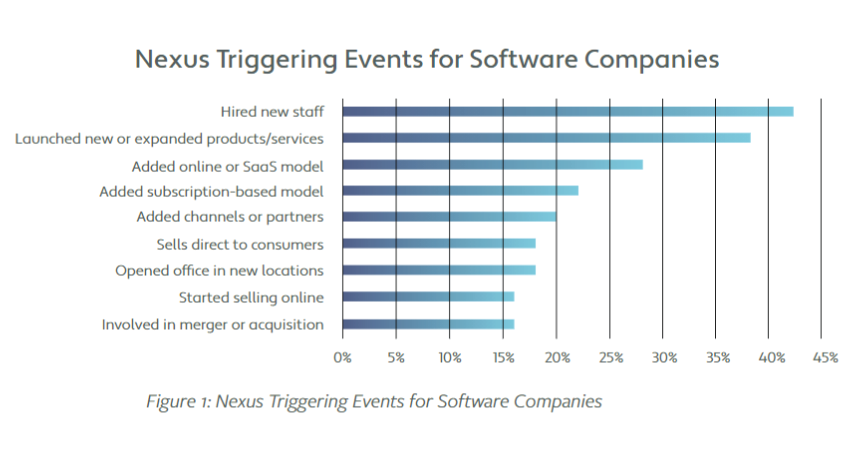

A survey conducted by Avalara and MKG found that, on average, software companies engage in nine activities that can trigger sales tax obligations (see figure 1). The most common activities are:

- Hiring employees and contractors in remote offices

- Launching new products

- Migrating products and/or services to the cloud

While these activities are common in many industries, software companies do them more often and at a faster pace. Yet accounting or finance teams may not intuitively realize that these activities now require the company to register to collect, remit, and file sales tax in more states.

The complex nature of software taxability

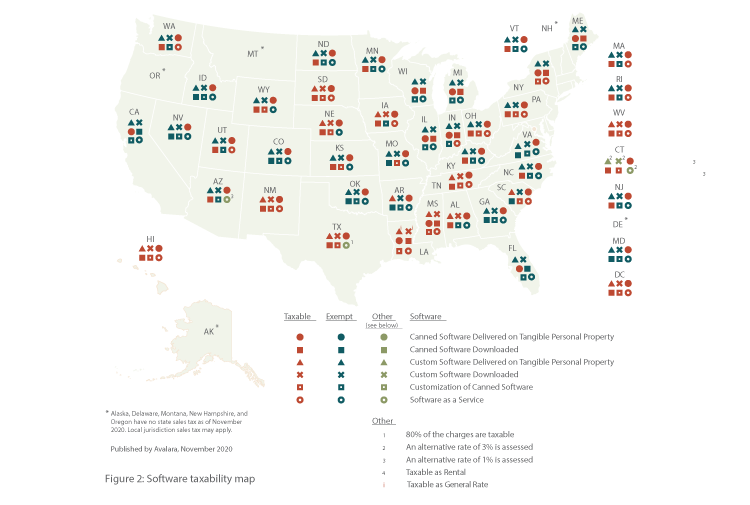

Taxability of software-related products and services is perplexing to say the least. Software is currently taxed in numerous different ways based on multiple distinct categories, including criteria such as physical or digital, custom or canned, software as a service (SaaS), or some combination thereof. To make matters worse, each state may make its own rules for how software is taxed or exempted (see figure 2).

To put this in perspective: Let’s say you launch a new product and plan to deliver it as both a digital download and an online service.

Fees for support and integration may be included, or those services might be available for purchase, along with licenses. Depending on the type of software, any services provided, and the distribution method, this single transaction could be taxed at very different rates based on where it was purchased, who purchased it, and whether it’s taxable or exempt or partially exempt according to state or even local jurisdiction rules. This is just one scenario not uncommon among software companies.

The SaaS model makes compliance even more complicated. The borderless character of SaaS delivery creates a tangle of taxability subject to sourcing rules in the jurisdictions of both the software vendor and the customer. Simply put, for any state where customers are buying your company’s software, there’s the potential to trigger new sales tax obligations. All this complexity means the compliance process for software companies is prone to error, inefficiencies, and risk.

In the software and technology industry, what’s taxed versus what’s not taxed can be counterintuitive.

- Web-based software is taxed in 19 states, partially taxed in 1 state, and taxed only if the provider has a server in that state in 5 states

- In Colorado, software services exempt from state sales tax may be subject to local sales taxes

- Digital movies are exempt from tax in 30 states, but video programming streamed over the internet is subject to tax in only 27 states

- Connecticut taxes digital movies and streamed video programming at the state sales tax rate of 6.35% unless they’re for “business use only,” when they’re taxed at a reduced rate of 1%

- Digital photography is generally taxed in 37 states, but digital photography associated with the sale of advertising services is only taxed in 23 states

- Digital games are taxed in 36 states when ownership is permanent, but only 30 states when it’s not

- Training associated with the sale of on-premises software is taxed in 10 states, but software training not associated with a sale is taxed in 6 states

- Hardware installation associated with the sale of tangible personal property is taxed in 23 states, but hardware installation not associated with a sale is taxed in 18 states

- Optional maintenance agreements associated with sales of downloaded software that include support services and updates are subject to sales tax in 29 states and partially taxed in 4 states, but optional maintenance agreements associated with software delivered on physical media that includes support services and updates are subject to sales tax in 36 states and partially taxed in 8 states

New nexus laws exacerbate the problem

Until recently, establishing a taxable connection to a state (nexus) required physical presence. Growth in online, remote, and cross-border transactions led many states to view the physical presence standard as outdated and inadequate, citing millions in lost revenue, and resulted in many states expanding sales tax nexus rules to include more online and offline growth-related business activities.

On June 21, 2018, the United States Supreme Court ruled in the case of South Dakota v. Wayfair, Inc. that states are within their constitutional rights to impose economic nexus, requiring remote sellers to collect and remit sales tax based solely on meeting certain thresholds for revenue and/or volume of sales into a state. To date, 43 states and the District of Columbia impose economic nexus.

So now, in addition to nexus triggers like remote employees, new products, and the like, you also have ecommerce sales to monitor, which can include software downloads but also licenses, support, training, upgrades, or other products or services you sell online.

Economic nexus, click-through nexus, and changes to physical nexus requirements have ushered in an inflection point for high-growth businesses, where indirect tax compliance is an integral piece of the business. It’s key to understand the tax implications of all your sales activities and a good place to start is with a nexus risk assessment, which can help you determine if you’re missing or overlooking any compliance obligations.

Nexus: The 800-pound gorilla of sales tax compliance

Nexus is a company’s connection to a state that warrants a tax obligation and it’s been a hot topic of debate in Congress and the courts for years. Historically, physical location determined whether a company collected and remitted sales tax to a state, but now with the boom of ecommerce, states are taking an aggressive approach in determining who owes sales tax.

Top nexus triggers for software companies:

- Expanding workforce (including contractors) in new locations

- Selling products and/or services in the cloud

- Launching new products and services

Major types of nexus:

- Physical nexus: established through physical locations, workforce locations (including contractors with a W-9)

- Economic nexus: established when sales into select states exceed threshold amounts

- Click-through or affiliate nexus: established by using online affiliates, such as resellers and online ad services

Sync your sales tax strategy with your five-year growth plan

A future-forward sales tax strategy actively addresses where you’re likely to grow next and simplifies tax responsibilities proactively. Consider how your company is likely to grow or change in the future. At each stage in that growth, sales tax compliance plays a role and adds complexity to the business. Before you entertain any big event, be clear on how it will impact your company’s ability to be compliant.

Malcolm Ellerbe, Tax Partner at Armanino LLP, frequently sees executives at fast-growing companies caught off guard by tax liabilities that weren’t on their radar. “Discovering large prior period liabilities during due diligence or by your financial statement auditors compounds an already complicated process,” says Ellerbe. “No executive wants to get caught flat-footed by the auditors or by the Board of Directors with something that can easily be mitigated early on.”

Start with a clean slate. If you’ve had issues with sales tax or audits in the past, remedy those right away. Then consider whether your growth plans could trigger any new obligations and how you’ll deal with those before they become a liability.

Selling online or through new sales channels

All U.S. states with sales tax, except Missouri and Florida, require online sellers to collect sales tax on ecommerce transactions if their economic activity in the state exceeds annual sales revenue or transaction volume thresholds. And more than 20 states have affiliate or “click-through” nexus laws that don’t require a physical presence to create tax liability; participating in affiliate programs or online advertising is enough to create that connection. For example, if an in-state online business leads a customer via links (“clicking through”) to buy something from the out-of-state online business, the out-of-state business is considered to have a presence in that state and must collect sales taxes from customers there. These nexus triggers, sometimes referred to as “Amazon laws,” can affect companies of all sizes, but high-growth software companies are primary targets because they’re primary users of online marketplaces, digital advertising, and internet referral programs.

Entering new markets or launching new taxable products or services

Growth-driven companies are always innovating, looking for ways to break into new markets or reach more customers. However, adding new products or services can make compliance tricky, especially in emerging industries like software where tax laws haven’t caught up with technology. Product and service taxability can be difficult to determine. And there’s little consistency from state to state. Some products or services are taxable in some states but exempt in others. Other products and services are “sometimes taxable,” adding another layer of confusion. As mentioned earlier, software is currently taxed in numerous ways based on multiple distinct categories. More and more states are also taxing services. The sourcing rules for determining obligations can be tricky, especially if you have contractors or outsource these services to third parties. It’s easy for high-growth companies to get tripped up by product and services taxability, especially when their focus is on how to add value to the business, not tax liability.

Expanding footprint (growth in workforce and locations)

Growth for software companies also means selling into new states, and each new state has its own rules for taxing software. States with multiple tax jurisdictions can be very challenging when it comes to sales tax calculations since these states may not only have thousands of jurisdictions but also various taxability rules for each and every service or product you sell. It’s imperative that you can adapt quickly to new tax rules as you expand. That’s just the domestic perspective. International commerce has skyrocketed in recent years, with the ability to sell goods and services online. When expanding abroad, companies face customs, duty, and import taxes, in addition to local tax like Value-Added Tax (VAT) in the U.K. or General Sales Tax (GST) in Canada. Large companies have entire departments for these functions. However, it’s not unusual for small to midsize businesses to ignore this aspect of their cross-border selling.

Undergoing a business change event (financing, mergers, acquisitions, audits)

Many software companies receive funding through VC backing or private investors, from mergers and acquisitions, or through an IPO. During these dynamic change events, tax compliance often takes a back seat to other priorities. That’s a mistake. Failing to get sales tax compliance right can have a negative impact on these key moments. Ellerbe works with many investor-backed organizations throughout the funding process. He calls software companies “inflection point” companies, as they have high year-over-year revenue growth and are now confronting big issues that could have been avoided. Many of these issues arise when a software company looks to acquire another business or gets ready for an IPO. Investors often ask what the plan is to address any potential tax issues and look at a company’s ability to scale in assessing its value. Employing current best practices and technology to address sales tax compliance matters just like it would for any other back-office function.

“Discovering large prior period liabilities during due diligence or by your financial statement auditors compounds an already complicated process. No executive wants to get caught flat-footed by the auditors or by the Board of Directors with something that can easily be mitigated early on.”

— Malcolm Ellerbe, Tax Partner, Armanino LLP

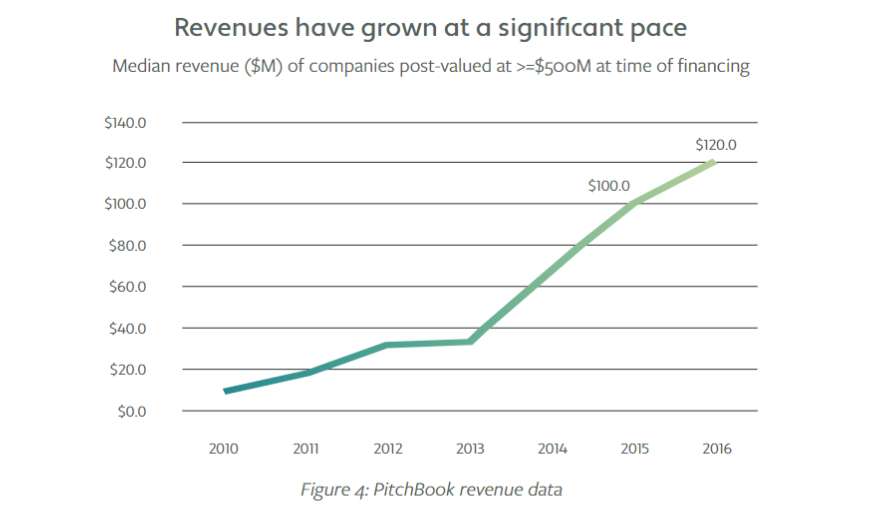

Research conducted by PitchBook shows that large, private VC-backed companies with fast-growing revenues have skyrocketed (See Figure 4).

The two primary exit strategies for these companies remain going public or being acquired, and both require even more extensive preparation than in the past given the current climate, especially if the given rate of growth has been quite rapid. Investors look hard at any potential financial liabilities that could impact the evaluation of the company.

Manual tax management isn’t sufficient

Rapid growth can quickly change your tax profile and liabilities, and the downstream effects of managing this change can impact operations. Having a sales tax compliance plan that grows with your business enables you to stay agile and avoid common pitfalls, such as frequent reassessments, fire drills, or worse, adding more resources into a non-revenue-generating activity.

The onerous processes associated with sales tax compliance makes it easy to deprioritize. The default reaction tends to be relegating sales tax to a line item for the accounting team, which typically involves hours spent on manual tasks, like researching rates and rules across more than 13,000 tax jurisdictions.

A survey of software companies conducted by Avalara and MKG found that 76% of software accounting and finance teams use manual processes to manage sales tax compliance. This includes everything from in-house CPAs researching government websites for tax policy information and rates to hiring outside tax experts to manage the process. According to Wakefield Research, the average company has six accounting professionals spending 39 hours a month on sales tax-related activities.

76% of software accounting and finance teams use manual processes to manage sales tax compliance

Source: Avalara-MKG Software Survey

A software solution for software companies

More software executives are starting to see the effects of inefficient sales tax management practices on the business and are looking for ways to remove compliance hurdles that could hinder growth.

For growth-driven companies, the ability to scale in key areas of the business is critical. This holds true for how you manage sales tax as well. Identify where you may have weaknesses now or in the future: Is IT being tasked with too-frequent requests to update sales tax rates and rules? Is audit risk higher because of new or pending product, service, or sales channel changes? Is your finance team bogged down trying to keep up with remittance and filing requirements in more states? Once you’ve exposed any Achilles’ heels that may be preventing growth, you can be objective and targeted in sourcing solutions.

This should be the tipping point to automate tax. Employing software to do the work of staff not only cuts down on errors and audit risk, it’s also more efficient. You’re less reliant on internal staff to manage sales tax, which means those resources can be reallocated to higher-value activities. Talk to your peers and platform provider. Ask them how they know they’re doing sales tax right. Explore cloud solutions like Avalara that are pre-certified to work with your ERP, accounting, ecommerce, point-of-sale, and billing systems or offer an API for easy setup and integration.